How to Calculate Car Loan Using Financial Calculator

TVM Auto Financing Car Loan Calculator

I. Introduction

In this guide, we’ll explore how to use the TVM functions on your financial calculator specifically for car loan calculations. You’ll learn how to determine monthly payments, calculate total interest costs, and compare different loan scenarios to find the most financially advantageous option.

II. Understanding Car Loans and TVM Variables

Before diving into calculations, it’s important to understand how car loans relate to the five key TVM variables:

Present Value (PV): This represents the loan amount or the price of the car minus any down payment. For car loans, PV is a positive value as it’s the amount you’re receiving from the lender.

Payment (PMT): This is your monthly car payment, which includes both principal and interest. For car loans, PMT is a negative value as it’s money you’re paying out.

Number of Periods (N): This represents the total number of monthly payments over the life of the loan. For example, a 5-year car loan would have 60 periods (5 years × 12 months).

Interest Rate (I/Y): This is the annual interest rate on your car loan. When calculating monthly payments, you’ll use the annual rate, and the calculator will convert it appropriately.

Future Value (FV): For a typical car loan that is fully amortized, the future value is zero, as the loan will be completely paid off by the end of the term.

III. Setting Up Your Calculator for Car Loan Calculations

Let’s use www.baiiplus.com for the example.

Before performing car loan calculations, ensure your calculator is properly configured:

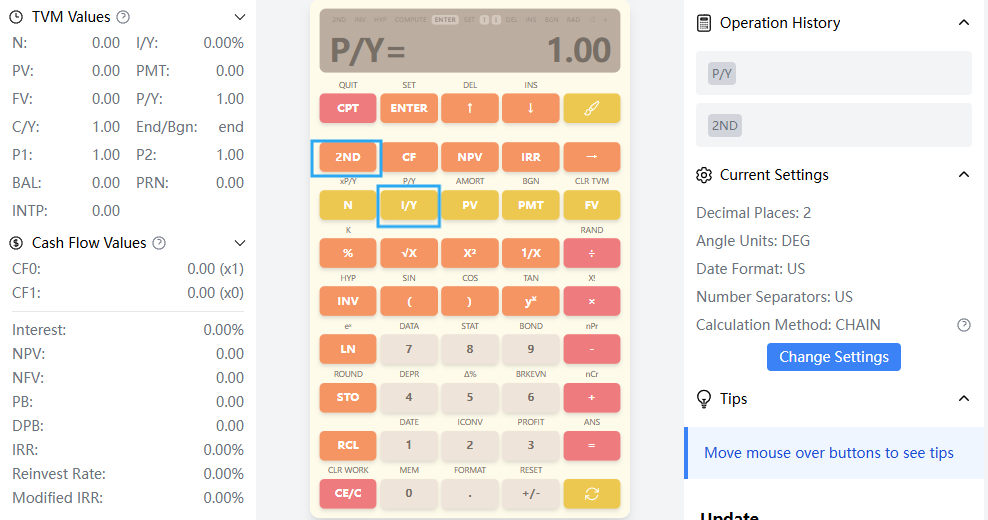

Set Payments Per Year: Press 2nd P/Y and enter 12 for monthly payments, which is standard for car loans. Press ENTER. The calculator will automatically set C/Y (compounding periods per year) to match P/Y.

IV. Calculating Monthly Car Payments

Example 1: Basic Car Loan Payment Calculation

You’re considering purchasing a car for $25,000. After a $5,000 down payment, you need to finance $20,000. The dealer offers a 4.5% interest rate for a 5-year (60-month) loan. What will your monthly payment be?

-

Clear TVM memory: Press 2nd CLR TVM(FV Key)

-

Enter the loan amount: 20000, then press PV (positive because you’re receiving this amount)

-

Enter the interest rate: 4.5, then press I/Y

-

Enter the loan term: 60, then press N

-

Enter the future value: 0, then press FV (the loan will be fully paid off)

-

Calculate the payment: Press CPT PMT

-

The calculator displays -372.86, indicating a monthly payment of $372.86 (negative because it’s money you’re paying out)

Example 2: Calculating Total Interest Paid

Using the same car loan from Example 1, how much total interest will you pay over the life of the loan?

-

Calculate the total amount paid: Multiply your monthly payment by the number of payments $372.86 × 60 = $22,371.60

-

Calculate the total interest: Subtract the loan amount from the total amount paid $22,371.60 - $20,000 = $2,371.60

This means you’ll pay $2,371.60 in interest over the 5-year term of the loan.

V. Comparing Different Loan Options

Example 3: Comparing Loan Terms

You’re considering two options for financing your $20,000 car loan:

- Option A: 4.5% interest rate for 5 years (60 months)

- Option B: 4.0% interest rate for 6 years (72 months) Which option results in lower monthly payments, and which option costs less overall?

For Option A (already calculated in Example 1):

- Monthly payment: $372.86

- Total paid: $372.86 × 60 = $22,371.60

- Total interest: $22,371.60 - $20,000 = $2,371.60

For Option B:

-

Enter the loan amount: 20000, then press PV

-

Enter the interest rate: 4.0, then press I/Y

-

Enter the loan term: 72, then press N

-

Enter the future value: 0, then press FV

-

Calculate the payment: Press CPT PMT

-

The calculator displays -312.89, indicating a monthly payment of $312.89

-

Calculate the total paid: $312.89 × 72 = $22,528.08

-

Calculate the total interest: $22,528.08 - $20,000 = $2,528.08

Comparison:

- Option A has higher monthly payments ($372.86 vs. $312.89) but costs less in total interest ($2,371.60 vs. $2,528.08)

- Option B has lower monthly payments but costs more in total interest over the life of the loan

This comparison illustrates an important principle: longer loan terms typically result in lower monthly payments but higher total interest costs.

VI. Calculating Affordable Car Price Based on Budget

Example 4: Maximum Affordable Car Price

You’ve budgeted $400 per month for a car payment. With a 4.5% interest rate and a 5-year (60-month) term, what price of car can you afford to buy after a $5,000 down payment?

-

Clear TVM memory: Press 2nd CLR TVM(FV Key)

-

Enter the payment amount: -400, then press PMT (negative because it’s money you’re paying out)

-

Enter the interest rate: 4.5, then press I/Y

-

Enter the loan term: 60, then press N

-

Enter the future value: 0, then press FV

-

Calculate the present value: Press CPT PV

-

The calculator displays 21,455.75, indicating you can finance approximately $21,456

-

Add your down payment to find the total affordable car price: $21,456 + $5,000 = $26,456

This means you can afford a car priced at approximately $26,456 with your $400 monthly budget, assuming a $5,000 down payment.

VII. Analyzing Early Payoff Scenarios

Example 5: Impact of Extra Payments

You have a $20,000 car loan at 4.5% interest for 5 years with a monthly payment of $372.86. If you decide to pay $450 per month instead, how much sooner will you pay off the loan, and how much interest will you save?

-

Clear TVM memory: Press 2nd CLR TVM (FV Key)

-

Enter the loan amount: 20000, then press PV

-

Enter the interest rate: 4.5, then press I/Y

-

Enter the payment amount: -450, then press PMT (negative because it’s money you’re paying out)

-

Enter the future value: 0, then press FV

-

Calculate the new term: Press CPT N

-

The calculator displays 48.71, indicating approximately 49 months.

-

Calculate the total amount paid: $450 × 49 = $22,050

-

Calculate the total interest: $22,050 - $20,000 = $2,050

-

Calculate interest savings: $2,371.60 (original interest) - $2,050 = $321.60

By paying an extra $77.14 per month, you’ll pay off the loan about 11 months earlier and save approximately $321.60 in interest.

VIII. Tips for Car Loan Calculations

-

Always clear TVM memory before starting a new calculation to avoid using values from previous calculations.

-

Double-check your inputs, especially the signs. For car loans, PV is typically positive (money you receive), while PMT is negative (money you pay out).

-

Consider all costs when entering the loan amount, including taxes, fees, and extended warranties that might be financed.

-

Compare APR, not just interest rates when evaluating loan offers, as APR includes certain fees and provides a more accurate comparison.

-

Remember that shorter loan terms generally result in higher monthly payments but lower total interest costs.

-

Factor in depreciation when deciding on loan terms. Ideally, you want to avoid owing more on the car than it’s worth (being “underwater” on the loan).

IX. Troubleshooting Common Issues

-

Sign Errors: Remember that in TVM calculations, cash inflows (money you receive) are positive, while cash outflows (money you pay) are negative.

-

Decimal Point Errors: Be careful with decimal points when entering interest rates. For example, enter 4.5 (not 0.045) for a 4.5% interest rate.

X. Conclusion

The TVM functions on your financial calculator are powerful tools for analyzing car loans and making informed auto financing decisions. By understanding how to calculate monthly payments, compare loan options, determine affordable car prices, and analyze early payoff scenarios, you can navigate the car buying process with confidence and potentially save thousands of dollars over the life of your loan.

Remember that while the calculator provides valuable financial insights, it’s also important to consider other factors such as reliability, fuel efficiency, insurance costs, and maintenance expenses when making your final car purchasing decision. The most financially advantageous choice is one that considers both the upfront financing terms and the long-term costs of ownership.